Welcome to Stuff I Thought About Last Week, a collection of topics on tech, innovation, science, the digital economic transition, the finance industry, cryogenic mirrors, and whatever else made me think last week. Please grab me on Twitter with any thoughts or feedback.

Click HERE to SIGN UP for SITALWeek’s Sunday EMAIL

In today’s post: ironic emojis; AI lacking analogizing; mobile gaming takes off while console/PC gaming plateaus; protecting consumers and labor vs. over regulating monopolies as the economy goes digital; making reality better; the James Webb Space Telescope; and much more below.

Stuff about Innovation and Technology

AI-Enhanced Mineral Prospecting

KoBold Metals is a material exploration company that flies a helicopter sporting a 115-foot-diameter copper coil to find deposits of cobalt and nickel for use in EVs and other tech devices: “These researchers plugged the new survey data into machine-learning models, which combined it with reams of other data the company has gathered to improve understanding of the region’s geology. Finally, they fed all this information into an artificial-intelligence system KoBold developed in partnership with Stanford University. The system draws on vast computational power to advise the team on the best places to survey next.” The new method is in contrast to the traditional way of manually analyzing field-collected data after the mining season. KoBold uses their data to acquire mining claims; so, if you see a strange copper thingy flying over your property, you might want to raise your asking price.

🤣➡️☠️:😕

The WSJ reports on the widening generational gap for interpreting emojis. A smiley face for the younger generation is now sarcastic and disingenuous. An LOL or a cry-laughing emoji is now a skull and crossbones...because they are dying laughing. With increased use of enterprise texting apps at work, the generational gap can lead to misunderstandings and miscommunications, according to the WSJ. Given the prevalence of text-based communication in the Information Age, a shift to a universal symbolic language sometimes seems inevitable to me. But, if one emoji becomes ironic to some and not to others, we might see a complete breakdown in our hieroglyph-ing. My go-to is always Emojipedia to check what something is supposed to mean; or, better yet, maybe we should just stop communicating altogether until Neuralink is available. PS: I am old.

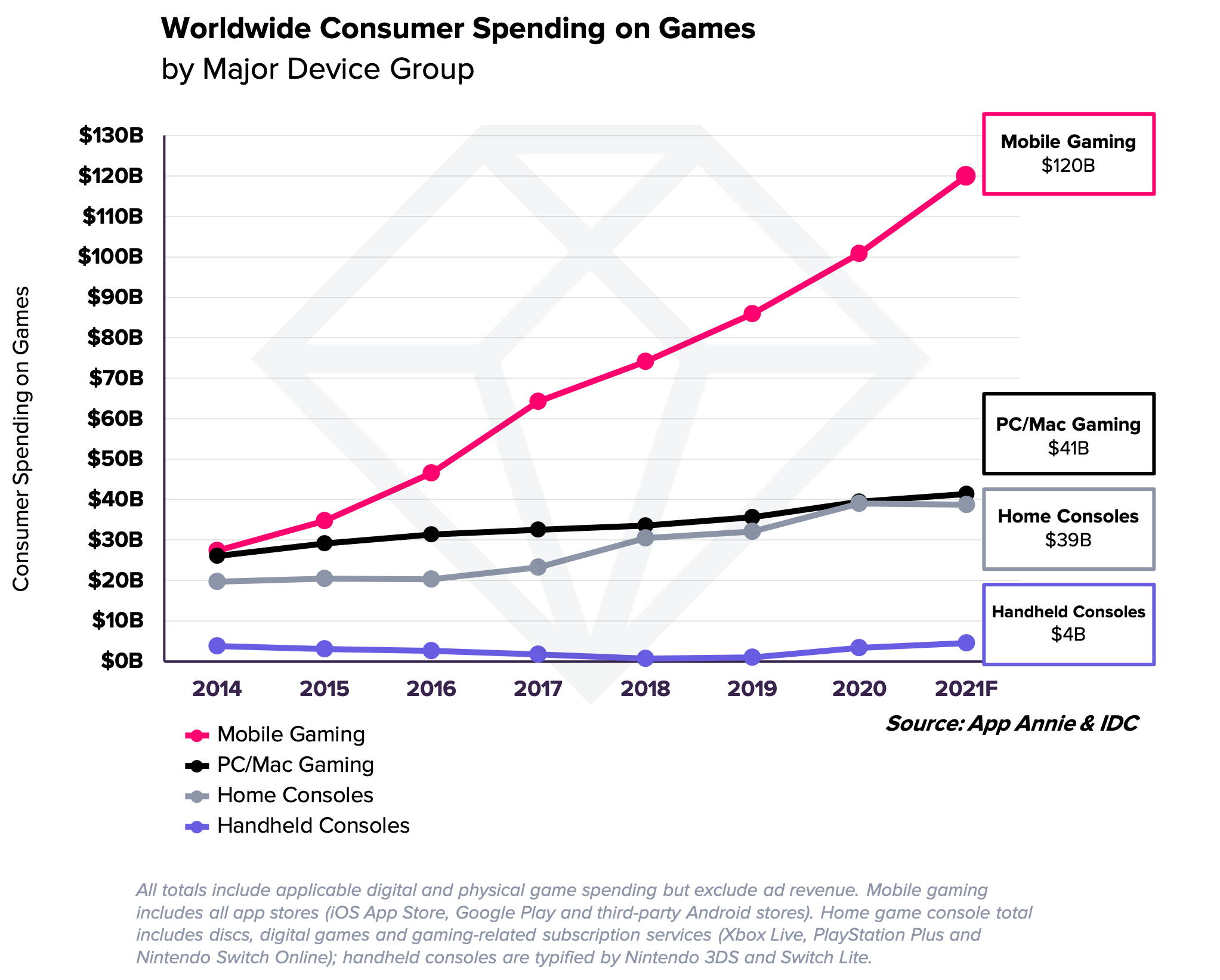

Mobile Madness

Mobile games are continuing their pandemic surge as App Annie is still predicting 20% growth in 2021 ($120B total by year’s end) following similar growth rates in 2020. This growth trend for mobile strikingly contrasts with that of console/PC gaming, which has been flatlining this year following meaningful growth in 2020. We’ll have to see how gaming behavior continues to evolve, but, at the moment, there seems to be a fairly large expansion of the casual, mobile gaming market due to increased phone usage that, like a bad habit, has stuck to post-lockdown life. Anecdotally, I see people using their phones in scenarios in which I don’t recall them being used pre-pandemic, suggesting the cigarette-like behavior is manifesting in increased mobile gaming and short-form video viewing. In related news, Axie Infinity, a Pokémon-Go-like game, has recently and rapidly achieved $1B of in-game NFT sales.

Omniversified PowerPoint

At Nvidia’s 2021 GTC keynote address earlier this year, CEO Jensen Huang briefly appeared as a virtual replica of himself, with his avatar mimicking both voice and appearance (see 1:02:29 to 1:02:56 in the video as he unveils their new DGX computing platform). Nvidia revealed last week that they built the virtual Jensen, his kitchen – and the rest of the keynote – inside the company’s Omniverse design software. While virtual Jensen is somewhat of a letdown, the blog post contains a 30-minute explanatory video with all the details and advantages of collaborating and building in a shared, virtual world.

App Stores Need Consumer Protections, Not Growth Inhibitors

If there is an important tool or service only available from one or two places that many people absolutely need to function efficiently in their job/life, then the providers of that tool/service are probably monopoly utilities and should be regulated as such. I am, of course, describing the Apple and Google app stores. Multiple transactional aspects controlled by the platforms (fees, payment options, data portability, and communications) are now under scrutiny, and there’s a new bipartisan bill (PDF) in the US that attempts to solve some of the problems developers are facing. Today, perhaps less than 10% of the global economy is digitally transacted; but, decades from now that number could be 90%, the bulk of which could be taking place via apps distributed by app stores on software (and in some cases hardware) that is controlled by only two companies (outside of China). You occasionally see a company like Snap say they are perfectly happy with the app store fees and control mechanisms, but I would posit that’s because those high fees and controls make it harder for new Snap competitors to scale up economically while relying on app stores for distribution. TikTok was able to rise to prominence and become the top downloaded app globally only because its parent company funded billions in losses.

Regulators Serving Up Food-Delivery Roadblocks

Grocery and restaurant delivery in the US is a hypothetical business model where, if you squint hard enough, you can imagine a scenario where vertical integration, subscriptions, purpose-built warehouses, advertising, and routed delivery eke out enough margin to make up for the labor cost transfer from the consumer to the business. The imaginary business model seems unlikely to succeed without meaningful horizontal and vertical consolidation, unless a winner-takes-all platform emerges that is heavily subsidized by advertising or some alternative business model (like Amazon Prime subscriptions). But, the state of the business today is sufficiently negative sum (taking more value from restaurants, stores, and drivers/shoppers than it creates for itself, resulting in unsustainable consumer surplus) that proposed mergers are drawing government scrutiny. The Information reports that the FTC is investigating the Uber partnership with Gopuff and that DoorDash may have abandoned a deal for Instacart due to potential regulatory concerns. As I’ve written about several times, the multi-trillion-dollar food industry appears ripe for analog-to-digital transformation. Typically, that means a small number of platforms will develop network effects and scale to create a viable business with value creation for all constituencies. However, regulatory action that prevents consolidation might completely kill this negative sum biz. That said, there are clear issues today with underpaid workers, and narrow restaurant/grocery margins are problematic. It may simply not be possible to transfer the labor cost from the shopper/eater to the merchant given that food is such a low-margin, highly-fragmented industry overall. Instead, the winners may be the companies that find niche segments of higher margin and convenience, or those who take share with the best array of digital and robotic tools to create better customer experiences.

Don’t Replace Reality, Augment It

These comments from John Hanke, CEO of Niantic (Google spin-out and maker of Pokémon Go and other AR games), struck a chord with me:

“I’m not denying that the metaverse is a cool concept from a technology point of view; it comes from one of my favorite sci-fi writers, Neal Stephenson, who coined the term in his 1992 novel, Snow Crash. Along with the works of William Gibson, that book created the cyberpunk genre, in which characters spend time wired into a digital universe where they explore, socialize, fight, and (at least in the novels) save the world from villainous plots. The concept reached one of its most complete expressions in Ernest Cline’s Ready Player One, where virtually everyone has abandoned reality for an elaborate VR massively multiplayer video game.

A lot of people these days seem very interested in bringing this near-future vision of a virtual world to life, including some of the biggest names in technology and gaming. But in fact these novels served as warnings about a dystopian future of technology gone wrong.

As a society, we can hope that the world doesn’t devolve into the kind of place that drives sci-fi heroes to escape into a virtual one — or we can work to make sure that doesn’t happen. At Niantic, we choose the latter. We believe we can use technology to lean into the ‘reality’ of augmented reality — encouraging everyone, ourselves included, to stand up, walk outside, and connect with people and the world around us. This is what we humans are born to do, the result of two millions years of human evolution, and as a result those are the things that make us the happiest. Technology should be used to make these core human experiences better — not to replace them.”

{kind=link}

Miscellaneous Stuff

Peering Back in Time with NASA’s Webb

After 25 years and $10B, the 7-ton James Webb Space Telescope (JWST) is nearing its launch into heliocentric orbit 1.5M km beyond Earth, from where it will take the deep space exploration helm from the 30-year-old Hubble. Once deployed, “eighteen hexagons of gold-coated beryllium mirror will open out, like an enormous, night-blooming flower. The mirrors will form a reflecting surface as tall and as wide as a house, and they will capture light that has been travelling for more than thirteen billion years.” The JWST will orbit in line with the Earth/Moon so the mirror array can be isolated from radiation generated (or reflected by) the Sun, Earth, and Moon via a tennis-court-sized parasol. To keep the telescope out of the shadow of the Earth/Moon, it will also orbit the 2nd Lagrange point (L2) on the far side of Earth perpendicular to its heliocentric orbit (see embedded animation). Ball Aerospace made the mirrors and cryogenic actuators that can move each mirror and curvature to within 1/10,000 the width of a human hair. The more light we can collect, the deeper and longer we can stare back into time – potentially 13.5 billion years – toward the beginning of the universe as we know it, some 14 billion years ago. Unlike the Earth-orbiting Hubble, which could be repaired and upgraded (Ball Aerospace fabricated instruments to fix its fuzzy focus, among other improvements), the JWST will be beyond our physical reach, so let’s hope for a flawless deployment.

Analogizing Key to AI Success

SFI professor Melanie Mitchell sees inability to analogize as one of the biggest hurdles to AI. Mitchell comments: “Today’s state-of-the-art neural networks are very good at certain tasks, but they’re very bad at taking what they’ve learned in one kind of situation and transferring it to another.” Analogy is the central skill needed for AI to predict the future, express common sense, and retrieve the relevant past information for a current situation, according to Mitchell. “One of the theories of why humans have this particular kind of intelligence is that it’s because we’re so social. One of the most important things for you to do is to model what other people are thinking, understand their goals and predict what they’re going to do. And that’s something you do by analogy to yourself. You can put yourself in the other person’s position and kind of map your own mind onto theirs...It’s essentially a way of making an analogy.”

Opaque AI Scoring Controls Opioid Dispensation

NarxCare is a US database designed to flag medical patients that may have opioid addictions; however, it’s unfortunately a textbook example of AI that is underdeveloped and overly trusted before it’s been vetted as serving an unbiased, useful purpose. The system can cause a complete denial of medical care for yourself if you happen to have a dog that is also on medication or if you have cancer. It seems that NarxCare could use a little analogizing.

Philip Morris to Make Respiratory Medications

Cigarette maker Philip Morris, considered only a “medium” ESG risk according to Sustainalytics, is looking to buy respiratory drug maker Vectura for over $1B. It seems to me that a cigarette giant treating respiratory ailments is highly analogous to an undertaker drumming up their own business. In a call back to the paragraph above, I hope I am using the right emoji here: ☠️

Stuff about Geopolitics, Economics, and the Finance Industry

Rocketing CVC

CB Insights reported VC investments by corporate internal venture investment divisions hit $79B in the first half of 2021, exceeding the $74B for all of 2020. I seem to recall similar surges (in what is a typically looser source of VC money) during prior investment cycle peaks. Global VC deals of all types totaled $288B in the first half of 2021, more than double the prior six months. It’s an astonishing record that highlights the free money burning holes in enterprise pockets. Looking at the ratio, corporate-backed deals were around 27% of total VC investments. During the last 6-month peak, back in 2018, corporate deals were a little under 20%.

Soros on Xi

George Soros had a well-articulated WSJ op-ed on Xi's plans to stay past his term limit and become a dictator in 2022: Xi "faces an important domestic hurdle in 2022, when he intends to break the established system of succession to remain president for life...He knows that his plan has many enemies, and he wants to make sure they won’t have the ability to resist him. It is against this background that the current turmoil in the financial markets is unfolding, catching many people unaware and leaving them confused...He doesn’t know how the financial markets operate, but he has a clear idea of what he has to do in 2022 to stay in power...Thus, his first task is to bring to heel anyone who is rich enough to exercise independent power. That process has been unfolding in the past year and reached a crescendo in recent weeks." I wrote more about the widening range of outcomes in China in #307.

Optimism and Awareness Revisited

Last week, I linked to Kevin Kelly’s excellent case for optimism. It was a popular subject for readers (including my comments on optimism vs. cynicism in investing), as was my short essay relating magicians and comedians to investors; so, for anyone who happened to be on vacation and missed it, you can read #308 here.

✌

Disclaimers:

The content of this newsletter is my personal opinion as of the date published and is subject to change without notice and may not reflect the opinion of NZS Capital, LLC. This newsletter is simply an informal gathering of topics I’ve recently read and thought about. It generally covers topics related to the digitization of the global economy, technology and innovation, macro and geopolitics, as well as scientific progress, especially in the fields of cosmology and the brain. I will frequently state things in the newsletter that contradict my own views in order to be provocative. Often I try to make jokes, and they aren’t very funny – sorry.

I may include links to third-party websites as a convenience, and the inclusion of such links does not imply any endorsement, approval, investigation, verification or monitoring by NZS Capital, LLC. If you choose to visit the linked sites, you do so at your own risk, and you will be subject to such sites' terms of use and privacy policies, over which NZS Capital, LLC has no control. In no event will NZS Capital, LLC be responsible for any information or content within the linked sites or your use of the linked sites.

Nothing in this newsletter should be construed as investment advice. The information contained herein is only as current as of the date indicated and may be superseded by subsequent market events or for other reasons. There is no guarantee that the information supplied is accurate, complete, or timely. Past performance is not a guarantee of future results.

Investing involves risk, including the possible loss of principal and fluctuation of value. Nothing contained in this newsletter is an offer to sell or solicit any investment services or securities. Initial Public Offerings (IPOs) are highly speculative investments and may be subject to lower liquidity and greater volatility. Special risks associated with IPOs include limited operating history, unseasoned trading, high turnover and non-repeatable performance.